Credit Reports: How to order, read and understand yours

(This page may contain affiliate links and we may earn fees from qualifying purchases at no additional cost to you. See our Disclosure for more info.)

Your credit report contains a great deal of information about your financial past:

- Your current and past debt balances

- How often you’ve missed payments

- Where you’ve applied for credit

- Information on bankruptcies and tax liens

- How far behind you are on child support

- Your previous addresses

- Previous employers and more

Since your credit report contains all of the above information, you can understand why it’s so important to review it regularly to verify its accuracy.

With others accessing your report from time to time – when you apply for credit cards, loans, employment, insurance, rentals, etc. – it's critical your report be accurate.

If it's not, you can risk job, housing, or financial opportunities or face potentially higher rates.

Additionally, you'll also want to check your credit report frequently to help protect yourself from identity theft. If your credit report shows accounts you didn’t open, you’ll know someone is committing fraud.

Keep reading to learn how to request, read, and understand the information you'll find in your credit report.

How to Order Your Credit Report For Free

Free Due to Federal Law

Thanks to the Fair Credit Reporting Act (FCRA), you can receive a free credit report from each of the three credit reporting bureaus (Equifax, Experian, and TransUnion) every 12 months.

You can order all reports at once or consider staggering them out by ordering from just one of the credit reporting agencies every 4 months.

Don’t fall for gimmicky commercials claiming you can get a free credit report. To do that, they make you sign up for a monthly service, which costs you money. That’s a bad idea.

The only place to obtain your free reports is the official site AnnualCreditReport.com which is run by all three credit bureaus.

You can also call 1-877-322-8228 or complete the Annual Credit Report Request Form and mail it to: Annual Credit Report Request Service, P.O. Box 105281, Atlanta, GA 30348-5281.

When completing your credit report request, be prepared to answer a few questions about your credit history.

You may get questions like “at what bank did you open up a mortgage?” or “which one of these streets did you live on?” They are pretty basic, but if you don’t know the answer to one, it may prevent you from receiving your report.

If you’ve already used all of your allotted FCRA credit reports in a year, there may be additional ways to receive your report for free.

Free Due to State Law

Some states allow their residents to receive another free report from each credit bureau. This is in addition to the three that you can receive from the FCRA. If your state isn’t on the free list, they may offer a discount which may be helpful.

For most states, in order to use this benefit, you need to contact each credit bureau directly. The annual credit report website above will not work. Here are the phone numbers for each credit bureau:

- Equifax – 1-888-548-7878

- Experian – 1-888-397-3742

- TransUnion – 1-800-916-8800

Additional Ways to Get a Free Credit Report

Here are some other ways to may be able to obtain your report for free:

- You’ve been denied credit, insurance or employment and you request your report within 60 days

- You’re unemployed and plan on looking for work within 60 days

- You’re on welfare

- Your credit report is inaccurate due to fraud or identity theft

For these instances, contact the credit bureaus directly.

How to Read and Understand Yours

Now that you have your credit report, it’s time to figure out how to read and understand the information in it.

Here is a list of things you’re going to find:

Personal Information

Your credit file will contain various types of personal information. Expect to see your:

- Social Security Number (it may only show the last 4 digits)

- Date of birth

- Current address

- Previous addresses

- Current and former employers (not always)

If you see any errors, be sure to contact the credit bureau for correction.

Your credit report will NOT contain any of the following, your:

- Salary

- Bank account balances

- Debts interest rate

- Credit counseling history

- Child support payments (unless you are delinquent)

- Race, religion, sex, marital status, etc.

Credit Summary

Some of the credit bureaus provide you with a credit summary. It shows the total number of open accounts, total current balances, total available credit, and monthly payment amounts.

Types of Credit Accounts

Typically, your credit report will list each of your accounts in one of four categories. They are as follows:

1. Mortgage Accounts

This is where you’ll find your first mortgage and any other loans secured by real estate.

2. Installment Accounts

These are credit accounts that have a predetermined payment and payoff date. This is where you would find your accounts for car loans, student loans, personal loans, or mortgages.

3. Revolving Accounts

Here you’ll find anything that has a credit limit and requires a minimum payment each month. Your credit cards will be the most likely items here.

4. Other Accounts

Very few people will have accounts listed in this category. It includes charge cards that must be paid in full each month and cannot carry a balance forward.

Information Reported For Each Account

Each account listed will have several different items reported on it. This is the heart of your report.

As you're going through these items, make sure each one is correct. If you find an error, take steps to get it corrected.

Creditor Name and Account Number

This is where you’ll find the name of the creditor and the associated account number.

Account Owner

Here you’ll see the ownership of the account (i.e., how you are associated with it). It could be one of these:

- Individual

- Joint

- Authorized User

- Co-Signer

Term Duration

If the account is on an installment payment plan, this is where you'll find the duration of payments. It’s typically listed in months.

Term Frequency

This defines how often you are required to make a payment, typically monthly.

Type of Loan

This defines the type of loan you have. It could say auto, education, mortgage, credit card, or charge card.

Credit Limit

If your account has a credit limit, it will be listed here. If the creditor has decided to reduce it, this limit may be less than your account balance.

High Credit

This is the highest your account balance has been since the account has been open.

Balance

Balances are typically reported at a specific time during the month depending on the creditor. The amount listed is the most recent balance reported on your account. It is NOT the high balance on your account during that given month.

In other words, if you charge $400 on your credit card and pay it off the next day, your reported balance could be reported as $0. It will be as if you didn’t even use your account.

Amount Past Due

If you neglect to make a payment by the required due date and it is still outstanding at the time the account was reported to the creditor, an amount will be listed here.

Scheduled Payment Amount

This is typically your minimum amount due on the account. It may be a billing cycle or two behind.

Actual Payment Amount

This is the most recent payment that has been posted to your account. It may be a billing cycle or two behind.

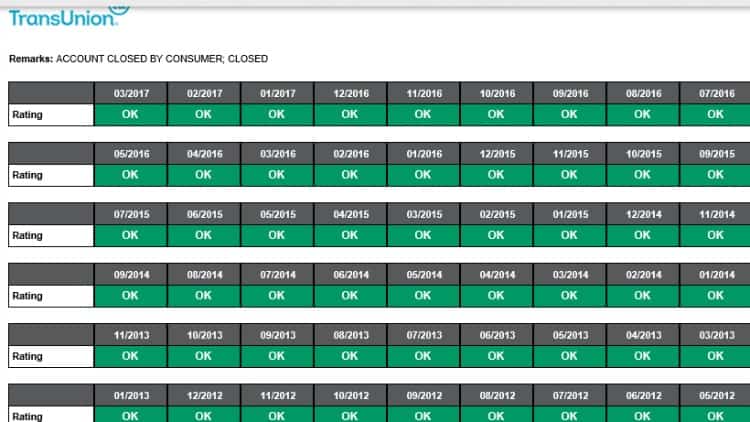

Payment History

The payment history section usually contains some type of chart or calendar. Each month will list if the account is current, 30, 60, or 90+ days past due.

Months Reviewed

This is the total number of months the creditor has reported information on your account. Even if the account is no longer open, a creditor could still report information.

Date Opened

This was when you opened the account.

Date of Last Activity

The last time you either added to the debt or made a payment.

Date Reported

The most recent date the creditor reported information regarding the account. If the account is closed, this could be a date several years ago as closed accounts can stay on your report for up to 7 years.

Date of Last Payment

This is the last time you paid on the account.

Date of 1st Delinquency

If you’ve had trouble paying your bills on time in the past, this is the date when the first issue happened.

Date of 1st Major Delinquency

If you do not pay your bill for 60+ days, an entry will be made here.

Charge Off Amount

If the creditor believes they will not be able to collect a debt from you, they may charge off your account. In other words, they will more than likely send your debt to a collection agency.

Date Closed

If you or the creditor decide to close your account to any new activity, you’ll find a date here. There’s usually something in the comments section listing who closed the account and for what reason.

Negative Accounts

If any of your accounts are past due or in collections, they will be listed in this section. These are the accounts you must thoroughly review for inaccurate information as they hurt your credit score.

Collection Accounts

If a creditor no longer feels they can get you to pay your account, they may sell your debt to a collection agency. The collection agency will then attempt to collect the past due amount directly from you.

Collection agencies have been known to go to extreme lengths to get you to pay. You should know your rights in those situations.

Public Records

This section contains information on bankruptcies, liens or judgments, and comes from federal, state, or county court records.

Credit Report Inquiries

When someone requests to view your credit report, it's logged and listed as an inquiry. There are two types of inquiries: hard inquiries and soft inquiries.

Hard Inquiries

Hard inquiries are ones you give authorization for.

When you’re applying for a loan, the creditor typically asks to view your credit report. When you authorize the request, this will count as a hard inquiry.

Hard inquiries may affect your credit score and prospective lenders can view them.

Soft Inquiries

Soft inquiries are all credit inquiries where a prospective lender is not reviewing your credit. They could include:

- Periodic reviews of your credit history by one of your current creditors

- Employment inquiries

- Checking your own credit report

- Promotional inquiries

Final Thoughts

Ordering, reading, and understanding your credit report takes time, but it's essential to do.

Your credit report is utilized in a lot of different ways and consistently reviewing the information for errors can save you a lot of money (and stress) over your financial life.

As mentioned above, some people order their reports from all three bureaus on the same day each year. Others choose to get one report every four months so they can check activity on their report more frequently.

The most important thing is that you check your reports at least once each year. And If you find any errors act immediately to get them corrected.

The FCRA requires both the credit reporting company and the party providing the information – the person, company, or organization giving the information about you to a credit reporting company – to correct inaccurate or incomplete information in your report. To take advantage of all your rights under this law, contact the credit reporting company and the information provider.

Written by Women Who Money Cofounders Vicki Cook and Amy Blacklock.

Amy and Vicki are the coauthors of Estate Planning 101, From Avoiding Probate and Assessing Assets to Establishing Directives and Understanding Taxes, Your Essential Primer to Estate Planning, from Adams Media.